What Reciprocal Trusts Are

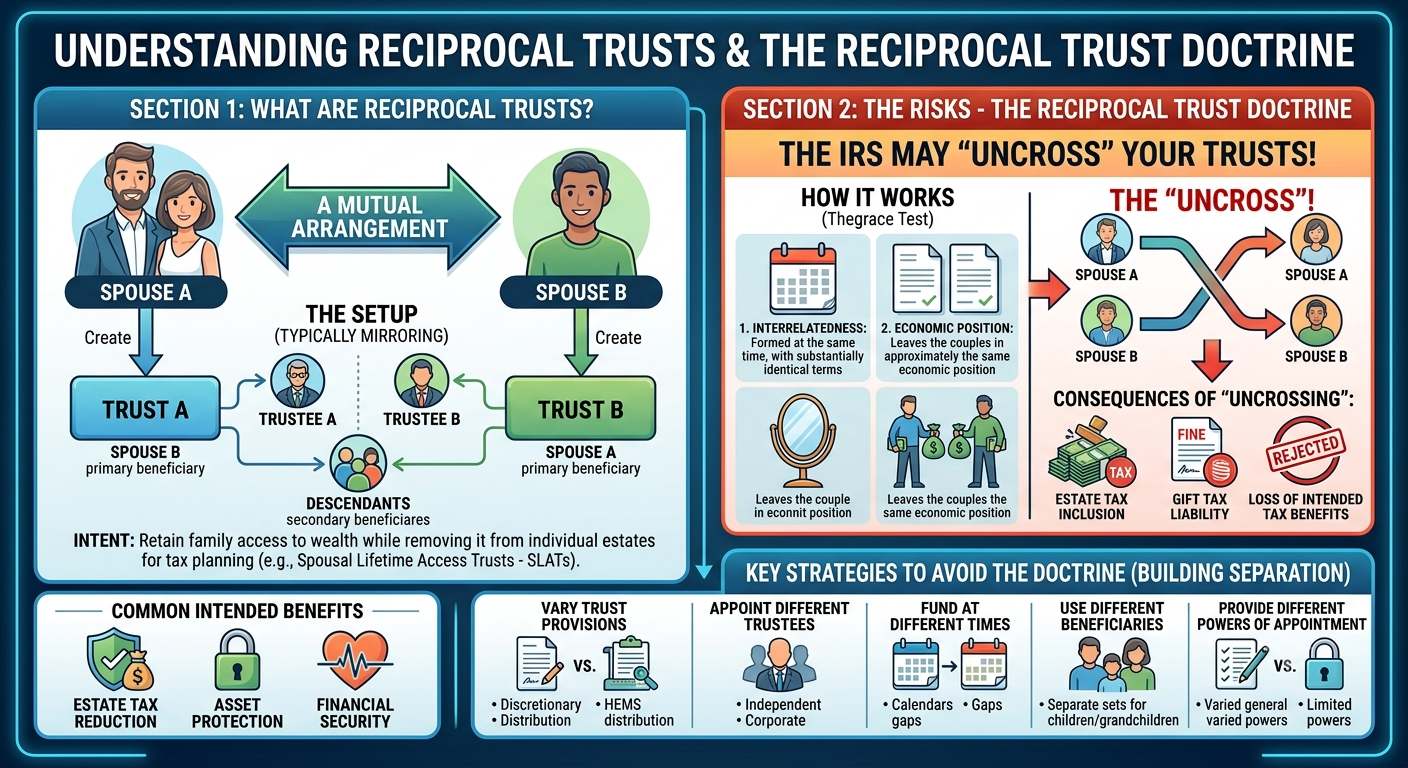

Reciprocal trusts — sometimes called crossed trusts or interrelated trusts — are two separate irrevocable trusts in which each party creates a trust for the other. In the most common arrangement, Spouse A creates Trust A naming Spouse B as a discretionary beneficiary, and Spouse B creates Trust B naming Spouse A as a discretionary beneficiary. The trusts are typically mirror images: they use the same distribution standards, the same or similar trustee provisions, and the same governing terms.

The word "reciprocal" captures the symmetry of the arrangement. Each spouse gives and receives in equal measure — Spouse A transfers assets to a trust that benefits Spouse B, and in exchange receives the benefit of a trust that Spouse B created. Because each grantor is a beneficiary of the other's trust rather than their own, neither appears to have retained a direct interest in the assets they transferred.

This distinction matters because it determines whether the trust achieves its purpose. An irrevocable trust in which the grantor retains no interest in the transferred assets can, if properly structured, remove those assets from the grantor's taxable estate and place them beyond the reach of the grantor's creditors. If the grantor retains a beneficial interest — or is treated as having retained one — neither benefit is available.

How Reciprocal Trusts Work

Each spouse executes a separate trust agreement as sole grantor. Because the trusts are irrevocable, the grantor relinquishes control over the assets at the time of funding — there is no reserved power to amend, revoke, or retake the property. This is the structural opposite of a revocable living trust, where the grantor retains complete control throughout their lifetime.

An independent trustee — someone other than either spouse — typically administers each trust. The grantor-spouse is excluded from serving as trustee of the trust they funded, because retaining trustee powers over one's own trust (such as the power to make distributions to oneself) can defeat the irrevocability of the transfer under the Internal Revenue Code.

During both spouses' lifetimes, each trust holds assets for the benefit of the other spouse under whatever distribution standard the trust document specifies — commonly a discretionary standard, a health/education/maintenance/support (HEMS) standard, or a combination. At the death of the beneficiary-spouse, the trust assets typically pass to children or other remainder beneficiaries as specified in the agreement.

Reciprocal trusts are not a standard or common arrangement for most couples. The complexity, irrevocability, and doctrine risk make them appropriate only when specific estate or asset protection goals justify the structure. For most Utah families, a joint revocable living trust accomplishes the core estate planning objectives without these complications.

The Reciprocal Trust Doctrine: When the Mirror Backfires

The reciprocal trust doctrine is a principle of federal estate tax law that addresses exactly the mirror-image arrangement described above. Its leading authority is United States v. Estate of Grace, 395 U.S. 316 (1969), in which the Supreme Court held that interrelated trusts may be "uncrossed" — treated for tax purposes as if each spouse had created a trust naming themselves as beneficiary rather than the other.

The practical effect of uncrossing is significant. Instead of each trust's assets being treated as a completed transfer to the other spouse (and therefore excluded from the grantor-spouse's taxable estate), the assets of each trust are included in the estate of the spouse who funded it — precisely as if that spouse had retained the assets outright. The estate tax benefit of the arrangement is eliminated entirely.

The doctrine applies when two conditions are met:

- The trusts are interrelated. They were created as part of a mutual plan, with each grantor aware of the other trust's creation. Simultaneous execution, coordinated funding, substantially identical terms, and shared legal counsel are all indicators of interrelation.

- Uncrossing leaves each grantor in substantially the same economic position. After uncrossing, does each grantor hold a beneficial interest in the trust they funded that is roughly equivalent to what they transferred? If Spouse A contributed $500,000 to a trust for Spouse B, and Spouse B contributed $500,000 to a trust for Spouse A under identical terms, uncrossing leaves each spouse with a $500,000 beneficial interest under terms they would have written for themselves — which is economically equivalent to having retained the assets.

The doctrine does not require that the trusts be literally word-for-word identical. Differences in the amount funded, the specific assets contributed, or minor variations in trustee succession provisions are generally insufficient on their own to defeat the doctrine if the trusts are otherwise clearly a coordinated plan and the economic positions are substantially equivalent.

The doctrine is about economic substance, not formal differences. The test from Estate of Grace is whether uncrossing the trusts restores each grantor to substantially the position they occupied before the transfer. Cosmetic differences in trust language do not change the economic reality if each grantor winds up with a beneficial interest materially equivalent to what they put in.

What Reduces Doctrine Risk — and What Doesn't

Because the doctrine looks to economic substance, reducing doctrine risk requires making the trusts meaningfully different in a way that changes each grantor's actual economic position — not just superficially different in drafting.

Approaches that can meaningfully reduce doctrine risk include:

- Different distribution standards. If Trust A uses a purely discretionary standard (the trustee decides whether and how much to distribute with no enumerated criteria) while Trust B uses an ascertainable HEMS standard, the two trusts give their respective beneficiaries different economic entitlements. This is one of the more effective distinctions.

- Genuinely independent trustees. Having the same institution or individual serve as trustee for both trusts strengthens the appearance of coordination. Naming different, unrelated trustees reduces it.

- Additional or asymmetric beneficiaries. If one trust includes children as primary co-beneficiaries with different share percentages or priorities, rather than simply naming the other spouse as the primary beneficiary, the trusts are no longer purely reciprocal in economic terms.

- Temporal separation. Creating the trusts at meaningfully different times — not as part of a simultaneous plan — weakens the "interrelated" prong. A trust created years before the other, for independent reasons, is harder to characterize as part of a mutual arrangement.

- Asymmetric funding. Funding the trusts with meaningfully different amounts or different classes of assets introduces economic asymmetry. Two trusts funded with identical dollar amounts from identical asset classes are difficult to distinguish economically.

- Different duration or remainder provisions. Trusts that terminate at different times, pass remainder to different beneficiaries, or grant different powers of appointment at termination have different economic structures even if the during-lifetime distributions look similar.

What does not reduce doctrine risk: minor variations in boilerplate trust language, slight differences in the names of successor trustees, or technical differences that do not change the economic substance of what each grantor will receive from the other's trust.

The Doctrine and Asset Protection — an Important Distinction

The reciprocal trust doctrine is a federal estate tax concept. It applies because of how the Internal Revenue Code treats retained interests — not because Utah state trust law categorizes the arrangement in any particular way.

For asset protection purposes, the relevant question under Utah law is different: can a creditor of the grantor-spouse reach the assets held in the trust? Because each trust is funded by a different grantor than the beneficiary, neither trust is technically a self-settled trust in the traditional sense — each grantor is creating a trust for someone else, not for themselves. Utah's domestic asset protection trust statute (Utah Code §§ 75B-1-301 through 310) governs self-settled trusts specifically, but a reciprocal arrangement sits in a different category.

That said, a creditor challenging a reciprocal arrangement may argue, by analogy to the reciprocal trust doctrine, that the economic reality of the arrangement leaves each grantor with a retained beneficial interest — and that the trusts should therefore be treated as self-settled for state law purposes. Utah courts have not extensively addressed this argument, and it represents an area of genuine legal uncertainty. The creditor protection benefit of a reciprocal arrangement is less well-established than the protection available under a properly structured Utah DAPT, and the two structures are not substitutes for each other.

Is a reciprocal trust or a Utah DAPT the right fit?

The difference matters — both for creditor protection and for how the assets are treated in your estate. A free consultation can walk through which structure accomplishes your specific goals.Reciprocal Trusts vs. a Joint Trust With Both Spouses as Trustors and Trustees

The most common alternative to reciprocal trusts for married couples is a joint revocable living trust in which both spouses serve as co-grantors and co-trustees. This is the standard trust structure for most Utah families and differs from reciprocal trusts in nearly every meaningful dimension.

| Feature | Reciprocal Trusts | Joint Trust (Both Spouses as Trustors/Trustees) |

|---|---|---|

| Number of trust documents | Two separate trust agreements | One combined trust agreement |

| Who creates the trust | Each spouse creates one trust, naming the other as beneficiary | Both spouses create a single trust together as co-grantors |

| Revocability | Irrevocable — cannot be amended or revoked after creation | Revocable — can be amended, restated, or revoked at any time during both spouses' lifetimes |

| Grantor's control over funded trust | None — grantor relinquishes all power over the trust they funded | Full — both spouses typically serve as co-trustees with authority to manage, invest, and distribute |

| Asset protection from creditors | Potentially — if properly structured, each trust may shield assets from the grantor-spouse's creditors; legal uncertainty applies (see above) | None while revocable — trust assets remain reachable by either spouse's creditors |

| Federal estate tax exposure | Subject to reciprocal trust doctrine — assets may be included in the grantor-spouse's estate if trusts are too similar | Assets included in grantor's estate (expected and unavoidable for a revocable trust; no planning purpose to avoid it) |

| Risk of reciprocal trust doctrine | Yes — must be carefully structured to minimize risk | None — doctrine does not apply to revocable trusts |

| Flexibility after creation | Very limited — irrevocable trusts can be modified only through judicial action or a named trust protector | Full flexibility — can reflect life changes, updated beneficiaries, or new planning goals at any time |

| Independent trustee required | Typically yes — grantor-spouse should not serve as trustee of the trust they funded | No — spouses serve as co-trustees without restriction during their lifetimes |

| Relative cost and complexity | Higher — two complex irrevocable instruments; ongoing independent trustee fees; greater drafting precision required | Lower — one document; spouses self-administer; amendment is straightforward |

| Best suited for | Couples with significant creditor exposure or estates approaching the federal exemption threshold who need irrevocable planning beyond what a DAPT covers | Most Utah couples whose primary goals are probate avoidance, organized succession, and disability planning |

When Each Structure Makes Sense

A joint revocable living trust is the appropriate structure for the vast majority of Utah married couples. It accomplishes the core estate planning objectives — avoiding probate, providing for disability, organizing the transfer of assets at death — with maximum flexibility and minimum complexity. Because it is revocable, the couple retains complete control throughout their lifetimes and can update the plan as circumstances change. The absence of asset protection during the couple's lifetimes is generally not a concern for families who are not in high-risk professions and whose estates are well within the federal exemption threshold.

Reciprocal irrevocable trusts warrant serious consideration for a narrower group of couples:

- Couples with significant creditor exposure. Business owners, licensed professionals in high-liability fields, and others who face meaningful risk of large judgments may benefit from irrevocable planning that places assets beyond their own creditors' reach during their lifetimes — a benefit a revocable trust cannot provide.

- Couples with estates that may approach the federal exemption threshold. The federal estate tax exemption is not permanent and has changed significantly over time. Couples who anticipate that their combined estates may approach the applicable threshold — particularly given the possibility of future exemption reductions — may have reason to consider irrevocable trust planning that removes assets from one or both taxable estates.

- Couples who have already used a Utah DAPT and need complementary planning. A Utah domestic asset protection trust and a reciprocal trust serve different purposes and are not competing tools. Couples who have already structured a DAPT may consider a reciprocal arrangement for assets held outside the DAPT, with the understanding that the two structures operate under different legal frameworks.

In each of these situations, the benefit of the reciprocal structure depends entirely on avoiding the reciprocal trust doctrine. If the trusts are too similar — in terms, timing, funding, and economic result — the doctrine will eliminate the estate tax benefit, and a creditor challenge based on similar reasoning may undermine the asset protection benefit as well. The arrangement is only worth pursuing when it can be structured with enough meaningful differences to withstand that scrutiny.

The mirror-image structure that makes reciprocal trusts intuitively appealing is the same feature that triggers the doctrine. The more precisely symmetrical the arrangement, the more likely it leaves each grantor in exactly the position they started in. Good planning in this area is built on intentional asymmetry — trusts that are coordinated enough to serve their purpose but different enough in economic substance to survive challenge.

Frequently Asked Questions

-

No. A joint revocable living trust is a single trust document in which both spouses serve as co-grantors and co-trustees. Reciprocal trusts are two separate irrevocable trusts — each spouse creates one, names the other as beneficiary, and has no retained control over the trust they funded. The structures are fundamentally different in revocability, control, asset protection, and cost.

-

The reciprocal trust doctrine is a federal tax principle, not a Utah state law rule. It applies in Utah — and everywhere else — because it arises under federal estate tax law, not state trust law. If a married couple in Utah creates two interrelated irrevocable trusts that leave each spouse in substantially the same economic position as if they had each retained the assets they transferred, the IRS may include those assets in each grantor's taxable estate under the doctrine established in United States v. Estate of Grace, 395 U.S. 316 (1969).

-

Potentially, but the structure must be carefully designed and the legal uncertainty is real. The reciprocal trust doctrine is primarily a federal estate tax concept — it does not directly determine whether assets are reachable by creditors under Utah state law. However, a creditor challenging the arrangement might argue by analogy that the economic reality of the arrangement leaves each grantor with a retained beneficial interest, which could affect the creditor protection analysis. Utah's domestic asset protection trust statute (Utah Code §§ 75B-1-301 through 310) provides a more established framework for self-settled asset protection trusts, though reciprocal trusts and DAPTs serve different purposes and are not substitutes for each other.

-

The core approach is to make the trusts meaningfully different in economic substance, not just superficially different in language. Effective differences include using different distribution standards (such as a HEMS standard for one trust and a purely discretionary standard for the other), naming genuinely independent and different trustees for each trust, including asymmetric beneficiaries or remainder provisions, creating the trusts at different times rather than as a simultaneous plan, and funding with meaningfully different amounts or asset types. No single difference guarantees the doctrine will not apply — the test is whether each grantor is left in substantially the same economic position as before the transfer.

-

For most Utah couples, a joint revocable living trust — in which both spouses serve as co-grantors and co-trustees — is the standard and appropriate structure. It avoids probate, organizes succession, provides for disability, and can be amended or revoked at any time. It does not provide asset protection during the couple's lifetimes, but that is rarely the primary concern for couples with typical estate sizes. Reciprocal irrevocable trusts are worth evaluating for couples with significant creditor exposure, estates that may approach the federal exemption threshold, or specific planning goals that a revocable trust cannot accomplish.