Two Programs, Two Entirely Different Sets of Rules

The first thing families need to understand is that "disability benefits" is not a single program with uniform rules. The two most common programs — SSI (Supplemental Security Income) and SSDI (Social Security Disability Insurance) — are governed by separate statutes, separate regulations, and separate eligibility criteria. Distributions from a special needs trust that are completely harmless under SSDI can meaningfully reduce SSI benefits. And because many disabled individuals receive both programs at the same time, the rules interact in ways that catch families off guard.

| Feature | SSI — Supplemental Security Income | SSDI — Social Security Disability Insurance |

|---|---|---|

| Governing statute | 42 U.S.C. §§ 1381–1383f | 42 U.S.C. §§ 401–434 |

| Needs-based? | Yes — limited income and resources required | No — based on work history, not financial need |

| Resource limit | $2,000 individual / $3,000 couple — 42 U.S.C. § 1382(a) | None |

| Income counted? | Yes — reduces monthly benefit dollar for dollar (after exclusions) | No income counting (only work activity matters) |

| In-Kind Support and Maintenance (ISM) rule? | Yes — food or shelter provided by others reduces SSI benefit | No ISM rule — shelter and food gifts have no effect |

| Cash from SNT reduces benefit? | Yes — counted as unearned income (after $20 general exclusion) | No effect on SSDI |

| Trust pays housing? | Reduces SSI via ISM rules (VTR or PMV) | No effect on SSDI |

| Trust pays supplemental items? | No effect if not food or shelter | No effect on SSDI |

| Associated health coverage | Medicaid (automatic in most states, including Utah) | Medicare (after 24-month waiting period) |

| What can end benefits? | Excess income or resources; moving out of needs-based eligibility | Substantial Gainful Activity (SGA) through work |

Why Even a Small SSI Benefit Matters More Than It Looks

When families learn that SSI pays a monthly cash benefit that is, for many recipients, under one thousand dollars, they sometimes wonder whether losing a portion of it is really a significant concern. The answer, in nearly every case, is yes — because the SSI benefit is not the only thing at stake.

In Utah and most other states, SSI eligibility is directly tied to Medicaid eligibility. Utah is a "1634 state," meaning it uses SSA's determination of SSI eligibility as the basis for Medicaid eligibility under 42 U.S.C. § 1396a(a)(10)(A). When SSI eligibility is disrupted — because resources or income exceeded the allowable limits — Medicaid eligibility can follow. For a person with a significant disability, Medicaid may cover personal care attendants, home health services, durable medical equipment, therapies, and the full cost of long-term care. That coverage often has a dollar value far exceeding the SSI cash payment.

This is why the rules for special needs trusts are not merely technical formalities. A trustee who makes the wrong kind of distribution — even with the best intentions — can inadvertently cost a beneficiary far more in Medicaid coverage than the value of whatever the trust paid for. This is one of several reasons housing and benefit questions belong in a broader disability planning conversation, not handled in isolation.

SSDI and Medicare are different. SSDI beneficiaries receive Medicare after a 24-month waiting period. Medicare is not Medicaid. Medicare requires premiums, deductibles, and copayments, and it does not cover all long-term care costs the way Medicaid does. Many individuals with disabilities rely on Medicaid — linked to their SSI — for coverage that Medicare alone would not provide.

How SSI Measures What a Beneficiary Receives

SSI eligibility and benefit amounts depend on two things: countable resources and countable income. Understanding how each is counted is essential to understanding what a special needs trust can safely pay for.

Resources

Resources are assets that a person owns and can use to meet their basic needs. Under 42 U.S.C. § 1382(a) and 20 C.F.R. § 416.1205, countable resources are limited to $2,000 for an individual and $3,000 for a couple. Certain assets are excluded under 42 U.S.C. § 1382b, including a primary residence (20 C.F.R. § 416.1212), one vehicle used for transportation, household goods, and properly structured trust assets that the beneficiary does not legally own or control.

A properly drafted third-party special needs trust is generally excluded from the SSI resource count under 42 U.S.C. § 1382b(e) and SSA POMS SI 01120.200, because the beneficiary does not own the trust assets and cannot compel distributions. This is what allows the trust to exist and grow without triggering a loss of SSI eligibility from the resource side.

Income

Income under SSI includes anything a person receives that can be used to meet needs, including earned income, unearned income, and in-kind support. A cash payment from a special needs trust directly to the beneficiary is unearned income under 20 C.F.R. § 416.1120 and is counted dollar-for-dollar against the SSI benefit after a $20 general income exclusion. If the trust pays $500 cash to the beneficiary in a given month, SSI is reduced by $480. For this reason, direct cash payments from a special needs trust to an SSI recipient are almost always a mistake.

In-Kind Support and Maintenance — The Rule That Governs Food and Housing

The most consequential rule for families thinking about housing — and the most misunderstood — is the In-Kind Support and Maintenance rule (ISM). Under 20 C.F.R. § 416.1130, ISM is any food or shelter that is provided to an SSI recipient, or that someone else pays for on their behalf. When a beneficiary receives ISM, their SSI benefit is reduced — not eliminated, but reduced by a fixed amount determined by one of two rules.

Rule 1: Value of the One-Third Reduction (VTR)

The VTR applies when an SSI recipient lives in another person's household and receives both food and shelter from that household. Under 20 C.F.R. § 416.1131, the SSI benefit is reduced by exactly one-third of the applicable Federal Benefit Rate (FBR) — currently $994/month for an individual — regardless of the actual market value of the support provided.

The VTR is the flattest and most predictable ISM reduction. When it applies, the $20 general income exclusion does not apply. A beneficiary living in a parent's home and receiving room and meals from the family will have their SSI reduced by one-third of the FBR each month, whether the family's home is modest or expensive.

Authority: 20 C.F.R. § 416.1131; see also SSA POMS SI 00835.400.

Rule 2: Presumed Maximum Value (PMV)

The PMV applies in all other ISM situations — when the beneficiary receives shelter (but not food) in another person's household, or when ISM comes from outside the household (such as a trust paying rent to a landlord). Under this rule, the SSI reduction is capped at the Presumed Maximum Value: one-third of the FBR plus $20. The reduction equals the lesser of the actual value of the ISM received or the PMV.

The PMV cap means that even if the trust pays expensive rent, the SSI reduction is limited. However, the beneficiary's SSI is still meaningfully reduced each month the trust is paying for shelter — and Medicaid eligibility tracks SSI eligibility.

Authority: 20 C.F.R. § 416.1140; see also SSA POMS SI 00835.500.

What "Shelter" Includes Under the ISM Rule

The definition of shelter under 20 C.F.R. § 416.1130(b) is broader than most people expect. Shelter includes:

- Rent payments

- Mortgage payments (principal and interest)

- Real property taxes

- Heating fuel

- Gas

- Electricity

- Water and sewerage

- Garbage collection

Importantly, several items that families often assume are "housing costs" are not shelter under the ISM rule and can be paid by a special needs trust without triggering ISM:

- Telephone and internet service — not shelter under the regulation

- Cable or streaming services — not shelter

- Renter's or homeowner's insurance — not listed as shelter in the regulation

- Furniture and appliances — not shelter (personal property, not the dwelling itself)

- Home modifications for accessibility — generally not shelter when made to improve the living space for disability needs

Paying any item on the "shelter" list from an SNT triggers ISM for that month. The VTR or PMV reduction applies for any month in which the trust makes a shelter payment on behalf of an SSI beneficiary. This is true whether the trust pays rent to a commercial landlord, a family member, or a housing authority.

SSDI and Special Needs Trust Distributions: No ISM Rules Apply

SSDI is an earned benefit program funded by the Social Security payroll tax. Unlike SSI, it is not means-tested. There are no resource limits, no income counting rules, and no ISM rules. A special needs trust can freely distribute cash, pay rent, cover grocery bills, or make mortgage payments on behalf of an SSDI recipient without any reduction in SSDI benefits.

The only thing that affects SSDI is Substantial Gainful Activity (SGA) — engaging in work that earns above the monthly SGA threshold established under 20 C.F.R. § 404.1574. Distributions from a trust, gifts of shelter, or family financial support do not constitute SGA. They have no bearing on SSDI eligibility.

For a family whose disabled member receives only SSDI — and whose SSDI income is high enough that they do not qualify for SSI — a special needs trust can be used very liberally, including for housing, without benefit consequences. The planning focus in that situation shifts to estate planning and asset management rather than benefit protection.

Concurrent Beneficiaries: When Both Programs Apply at Once

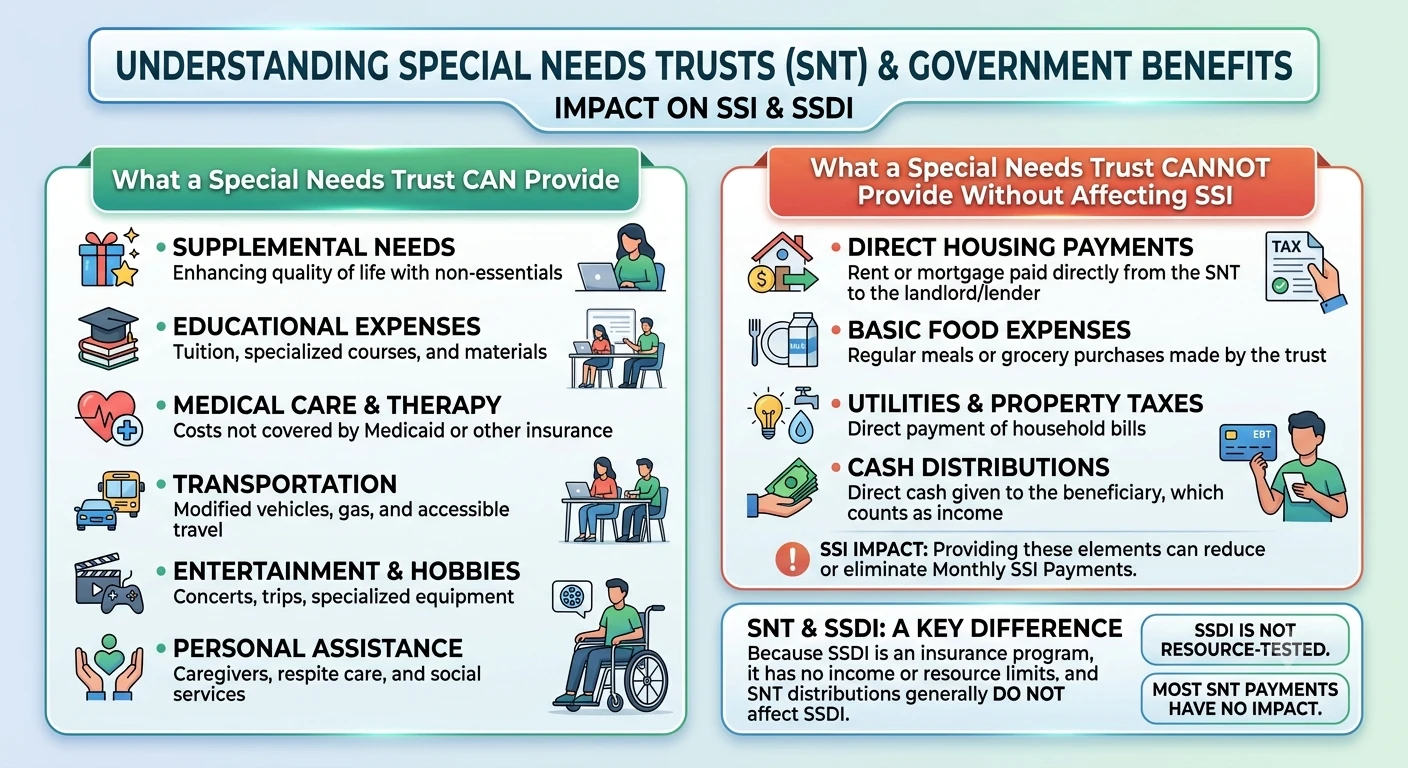

Many disabled individuals receive both SSI and SSDI at the same time. This happens when a person qualifies for SSDI but the SSDI payment is low enough — and their resources are limited enough — that they also qualify for SSI to supplement the SSDI payment. The SSDI is counted as unearned income for SSI purposes, reducing the SSI benefit, but the person remains eligible for both.

For concurrent beneficiaries, the SSI rules — including the ISM rules — still apply in full to the SSI portion of their benefits. A trustee cannot ignore ISM rules simply because the beneficiary also gets SSDI. Losing SSI, even a small SSI payment, can mean losing Medicaid — particularly important for concurrent beneficiaries who depend on Medicaid for personal care services that Medicare does not cover.

Is your disabled family member receiving SSI, SSDI, or both?

The right trust structure — and the right distribution decisions — depend on which programs the beneficiary receives. The first conversation with Paul is always free.What a Special Needs Trust Can Pay For

When a special needs trust pays for goods or services that are neither food nor shelter, those payments generally have no effect on SSI. This is the principle that makes SNTs useful: the trust supplements government benefits by covering everything the government does not, without reducing what the government provides.

Generally Safe for SSI Recipients

- Education, tutoring, and vocational training

- Recreation, hobbies, and entertainment

- Computers, tablets, phones, and communication devices

- Transportation (vehicle purchase, rideshare, adapted vehicle modifications)

- Medical and dental care not covered by Medicaid

- Therapy not covered by Medicaid (speech, OT, PT, behavioral)

- Personal care attendants beyond what the state provides

- Accessibility modifications to the home

- Telephone and internet service

- Clothing and personal items

- Vacation and travel expenses

- Companion animals and related care

- Prepaid funeral and burial expenses

- Legal fees on behalf of the beneficiary

Avoid or Use Extreme Caution

- Cash directly to the beneficiary — unearned income; reduces SSI dollar-for-dollar after $20 exclusion

- Rent or mortgage payments — ISM; reduces SSI by VTR or PMV

- Utility bills covered by ISM definition — gas, electricity, water, sewerage, heating fuel — ISM; reduces SSI

- Real property taxes paid by trust — ISM; reduces SSI

- Grocery purchases or food — ISM; reduces SSI

- Restaurant meals — food; may count as ISM

- Gift cards redeemable for food — treated as cash or food income

- Anything duplicating a covered government benefit — may count as income

The Housing Problem — and Approaches That Work

Housing is the issue that most families struggle with, and for good reason: disabled individuals often cannot live independently, and family members naturally want to help ensure they have stable, safe shelter. The challenge is that every form of housing assistance — whether rent paid by the trust, a family member allowing a child to live at home, or a trust purchasing a house — has SSI consequences that must be understood before the arrangement is set up.

There is no approach that eliminates the ISM problem entirely for SSI recipients in every situation. But several strategies manage it well.

Accept the VTR and Plan Around It

If a family member provides both housing and meals to the beneficiary in their household, the VTR applies and SSI is reduced by one-third of the FBR — not eliminated. This is a fixed, predictable reduction. The SNT pays for all supplemental needs. The beneficiary retains reduced SSI and, critically, retains Medicaid. For many families this is the simplest and most sustainable arrangement.

Purchase a Home and Transfer Title

If the SNT (or a family member) purchases a home outright and then transfers clear title to the beneficiary, the home becomes the beneficiary's primary residence — an excluded resource under 20 C.F.R. § 416.1212. Once the beneficiary owns the home free and clear, the trust does not need to make ongoing mortgage payments, eliminating that ISM. The trust pays for supplemental expenses only. This requires careful planning around the beneficiary's legal capacity to hold title, property taxes, and ongoing maintenance costs.

Charge Fair Market Rent

A beneficiary who pays fair market value rent for their housing — whether to a landlord, a family member, or a housing authority — is not receiving ISM, because they are paying for the shelter they receive. If the SNT's design allows the trustee to distribute income to the beneficiary for living expenses (a more liberal trust design), and the beneficiary uses that income to pay rent, no ISM is triggered. This involves careful coordination between the trust and the beneficiary's monthly budget, and must be structured to avoid the distribution itself being treated as income.

Limit Trust Payments to Non-Shelter Items

For beneficiaries living in any housing situation, the trust should generally limit its payments to items outside the ISM definition: phone, internet, clothing, recreation, therapy, transportation, and similar supplemental expenses. If the family or other arrangements cover shelter, the trust stays out of the ISM category entirely and the SSI benefit is preserved at full or near-full levels.

Example — VTR Situation: James has autism and lives with his parents in their home in Utah. His parents provide his room and all his meals. James receives SSI at the current Federal Benefit Rate of $994/month and Medicaid. The VTR applies: his SSI is reduced by one-third, to approximately $663/month. He retains Medicaid.

His grandparents establish a third-party special needs trust funded with $200,000 from their estate. The trustee pays for James's iPad, speech therapy sessions not covered by Medicaid, annual family vacations, adaptive sports equipment, phone plan, and a communication application subscription.

None of these payments are shelter or food. James's SSI remains at the VTR-reduced level. His Medicaid is unaffected. The trust improves his quality of life without reducing his benefits any further.

Example — SSDI-Only Situation: Sandra has multiple sclerosis and worked as a nurse for twenty years before becoming disabled. She receives $2,400/month in SSDI. Her income is too high to qualify for SSI. She has Medicare but relies on Medicaid for a personal care attendant because Medicare does not cover that service.

Her parents establish a special needs trust. The trustee pays Sandra's rent, covers her grocery deliveries, and pays her gas and electric bill.

None of these payments affect Sandra's SSDI. There are no ISM rules for SSDI. However, if Sandra also receives Medicaid (through a Medicaid waiver program separate from SSI), the trustee should confirm whether that Medicaid program has its own income or resource rules — some waiver programs do.

A Note on First-Party and Pooled Special Needs Trusts

This post has focused primarily on third-party special needs trusts — those funded by someone other than the beneficiary. But the ISM rules apply the same way to first-party trusts (self-settled trusts funded with the disabled person's own assets, such as a personal injury settlement, governed by 42 U.S.C. § 1396p(d)(4)(A)) and to pooled special needs trusts (administered by nonprofit organizations under 42 U.S.C. § 1396p(d)(4)(C)). A trustee of any type of SNT who pays shelter costs for an SSI recipient triggers ISM.

The primary distinction between trust types is not what they can pay for — it is who funded them and what happens to the remaining assets when the beneficiary dies. A first-party trust requires a Medicaid payback provision; a third-party trust does not.

Frequently Asked Questions

-

For a beneficiary who receives SSI, trust payments for rent, mortgage payments, utilities, or other shelter costs count as In-Kind Support and Maintenance (ISM) under 20 C.F.R. § 416.1130. ISM reduces the SSI benefit by either one-third of the Federal Benefit Rate (the Value of the One-Third Reduction) or the Presumed Maximum Value, depending on the living situation. Paying shelter costs from the trust is not prohibited — but it reduces the SSI benefit and should generally be avoided unless the strategy is carefully designed. For SSDI-only beneficiaries, there is no ISM rule and trust payments for housing have no effect on benefits.

-

In-Kind Support and Maintenance (ISM) is any food or shelter that is provided to an SSI recipient — or paid for on their behalf — by someone other than the recipient. Under 20 C.F.R. § 416.1130, shelter includes rent, mortgage payments, real property taxes, heating fuel, gas, electricity, water, sewerage, and garbage collection. When an SSI recipient receives ISM, their monthly benefit is reduced by either the Value of the One-Third Reduction (if living in another person's household and receiving both food and shelter) or the Presumed Maximum Value (in other ISM situations).

-

No. SSDI is not a needs-based program. It does not have resource limits, income counting rules, or In-Kind Support and Maintenance rules. Distributions from a special needs trust — whether cash, food, or housing — have no effect on SSDI benefits. The only thing that can reduce or end SSDI is engaging in Substantial Gainful Activity, which means earning above the SGA threshold through work. Trust distributions, gifts of shelter, and family financial support do not constitute SGA.

-

If an SSI recipient lives in another person's household and receives both food and shelter from that household, the Value of the One-Third Reduction (VTR) applies. The SSI benefit is reduced by exactly one-third of the Federal Benefit Rate — not eliminated, but meaningfully reduced. If the recipient receives only shelter (but not food) from the household, or receives shelter from outside their household (such as a trust paying rent to a separate landlord), the Presumed Maximum Value rule applies instead, capping the reduction at one-third of the FBR plus $20.

-

A special needs trust can purchase a home. If the trust owns the home and allows the beneficiary to live there without paying rent, that constitutes in-kind support and maintenance — the beneficiary is receiving shelter from the trust — and the SSI benefit will be reduced accordingly. One planning strategy is to have the trust purchase the home and then transfer clear title to the beneficiary. Once the beneficiary owns the home as their primary residence, it is excluded from countable resources under 20 C.F.R. § 416.1212. The trust can then pay for non-shelter expenses without triggering ISM. Each situation is fact-specific and requires careful legal review.

-

A special needs trust can pay for a wide range of goods and services that supplement — rather than replace — what SSI and Medicaid provide, without affecting the SSI benefit. These include education, tutoring, and job training; recreation and entertainment; technology such as computers, tablets, and communication devices; transportation; therapy and medical care not covered by Medicaid; personal care attendants beyond what the state provides; home accessibility modifications; vacation and travel; clothing; telephone and internet service; and prepaid funeral expenses. These items are not food or shelter and do not constitute ISM.

-

SSI (Supplemental Security Income) is a needs-based program that pays a monthly benefit to disabled individuals with limited income and resources, regardless of work history. It is governed by 42 U.S.C. §§ 1381–1383f. SSDI (Social Security Disability Insurance) is an earned benefit program that pays monthly benefits to disabled individuals who have accumulated sufficient work credits. It is governed by 42 U.S.C. §§ 401–434. SSI has strict income and resource rules, including ISM; SSDI does not. Many disabled individuals receive both programs simultaneously — in that case, SSI rules apply to the SSI portion and must be followed carefully.